Finance

2.4 Contribution & break-even analysis

Contribution

- The giving or supplying as a part or share of the total.

- Contribution per unit = Price – Average Variable Cost

Profit formula

- Profit = Quantity x Price - (Fixed Costs + (Average Variable Cost x Quantity))

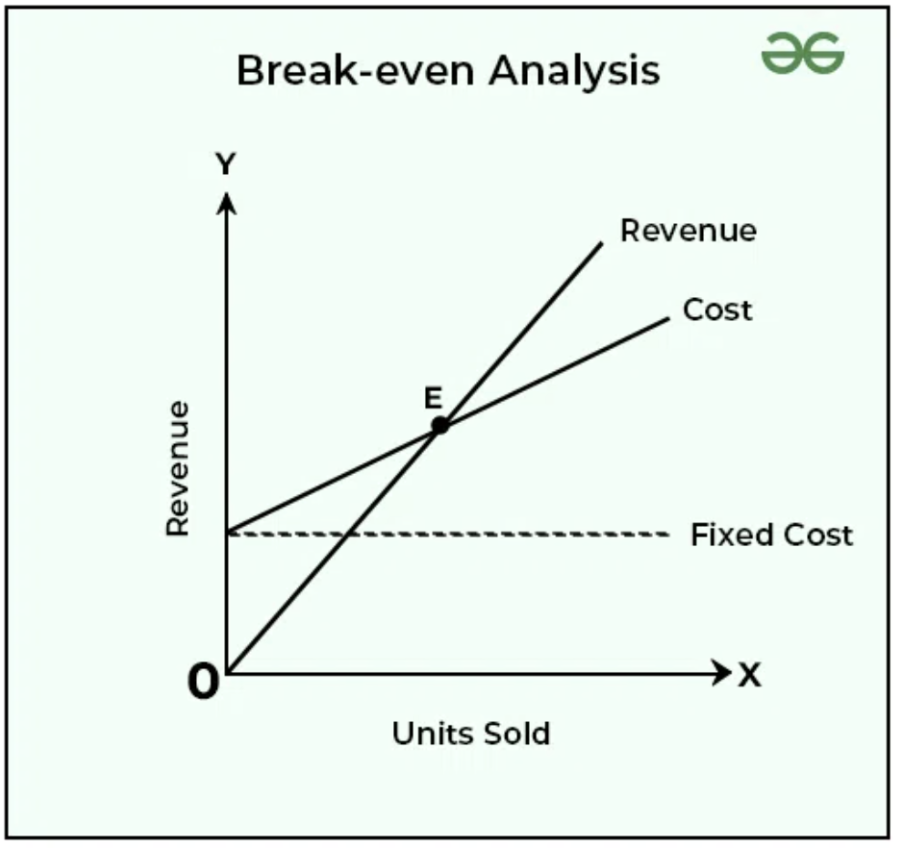

Break-even analysis

- It is where profit = 0, meaning the revenue covers the costs.

- Step by step to calculate and graph the break-even chart:

- Write profit equation = 0 ; 0 = Quantity x Price - (Fixed Costs + (Average Variable Cost x Quantity))

- Rearrange equation to find the unknown Quantity (the values will be given in question).

- After quantity value is found, calculate Quantity x Price to find the revenue.

- Plot a graph with Quantity in the x-axis and Revenue in the y-axis.

- Mark the break-even point (point with the Quantity and Revenue values that you calculated in step 2 and 3).

- Draw a line from 0,0 that passes through the break-even point and continue it until the end of the graph's axes.

- Draw the fixed cost curve (straight horizontal line with the value of fixed cost given in question).

- Draw total cost line starting at the fixed cost line and passing through the break-even point, and continue it until the end of the chart's axes.

- Write a title for the chart; e.g. break-even analysis for ____ at date ______.

- Remember to label the axes of the graph.

- Remember to label each line of the graph and the break-even point.

- it should look like this:

Margin of safety

- The difference between current/forecasted sales and the quantity of sales at breakeven point.

- output – breakeven point quantity.

Author: Felipe Rodrigues

Contact: fr1@stpauls.br