Finance

2.7 Efficiency ratio analysis (HL only)

Efficiency ratios

Measures how well the resources of a business are used in order to generate income from the firm's capital

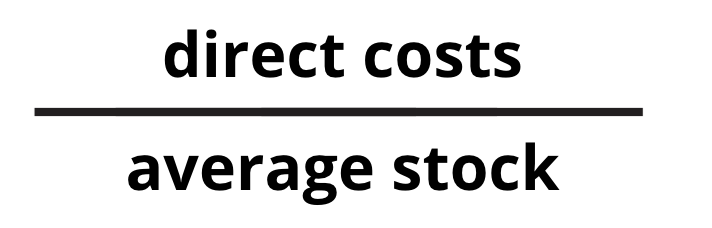

Stock turnover ratio

- Measures the number of days it takes for a business to sell its stock. It can also be manipulated to show the number of times during a given period of time that a business needs to restock. To find this simply divide 365 by stock turnover ratio (version: number of times).

- To improve ratio:

- Decrease stock focus on fast-moving products

- Forecast demand of products

- Increase COGS while maintaining inventory quantity (e.g., increase sales -> raw materials)

- Formula (number of times):

Debtor days

- Measures the average number of days an organization takes to collect its debts from its customers who have bought goods/services on trade credit. Businesses aim to have a low value.

- To improve ratio:

- Incentivize customers to pay with cash rather than credit

- Shorten credit period given to customers

- Formula:

Creditor days

- Measures how long it takes the company to settle the debts that it owes. Companies aim for a high value; more time to pay debts -> improves cash flow and working capital.

- To improve ratio:

- Negotiate with suppliers an extended credit period

- Look for other suppliers with better trade credit terms

- Formula:

Gearing ratio

- Measures how much of the capital employed of a company is financed by long-term loans

- Highly geared = +50%

- Normal gearing = 25-50%

- Low gearing = 25% or less

- Companies aim to not be highly geared as you are highly dependent on banks and other creditors for financing and can lead to significant amounts of interest

- Companies aim to not be low geared as it means there is low capital employed. This indicates that the business is not efficiently using all the venues available to grow (e.g., using loans to expand)

- Companies aim to be normal geared

- To improve ratio:

- Pay off some of the firms' long-term liabilities

- Give incentives for debtors to pay earlier

- Use internal sources of finance (to decrease) or use external sources of finance (to increase)

- Formula:

Exam tip

There is no need to memorize these formulas as they are given in the formula booklet

Insolvency vs Bankruptcy

- Insolvency is when an individual or business is not able to pay its debts but bankruptcy is when a business is insolvent so it files a legal process that may give it a chance to restructure its operations and debts and get back on its feet (become profitable)

- A business that is insolvent is not necessarily bankrupt but a business that is bankrupt is insolvent